The Token Bull Case: A Study on Revenue, POL, and the Next Token Era

In collaboration with Arrakis Finance, we explain why tokens will need revenue and Protocol Owned Liquidity to achieve long-term sustainability.

Obol is placing focus on revenue generation and Protocol Owned Liquidity moving forward because we believe that both will be essential for survival in the next era of tokens.

Are Tokens Dead?

The token market has endured a gruelling winter. Most assets in the market struggled over the last cycle despite Bitcoin’s sustained break above $100,000. Following the number one crypto’s new high in early Q4, the 10/10 meltdown broke the token market structure, sending many assets to new cycle lows.

By now it’s widely understood why most tokens were suffering even before 10/10. This was the cycle where the market woke up to the low float, high FDV games that enriched insiders in the 2021 boom. It was also the one that saw BTC gain institutional approval as digital gold while tokens were battling with an anti-narrative, leaving most to bleed against it.

The number of longtail assets on the market has also exploded since their late-2021 peak, fragmenting liquidity and creating decision fatigue among would-be holders. As tokens entered a years-long slump, the industry debated whether value would eventually accrue as equity to parent labs rather than tokens (though the likes of Aave and Uniswap have cast doubt on this narrative). The recent speculative fervor in the AI and precious metals markets has only strengthened the consensus view that tokens are dead.

Arrakis’s recently-published A Practical Guide to TGE in 2026 highlighted these points with hard numbers. It found that 85% of tokens launched in 2025 ended the year negative, with early underperformance reliably predicting continued underperformance. In the study, Arrakis also makes the case that DEX-first launches benefit many teams over CEXs and building a robust liquidity strategy is essential.

There is a future for (some) tokens. But “alt szn” is dead.

CEXs have played a role in the token market’s decline. Token issuers must pay high rental costs to secure CEX listings and they have to trust the parties they engage with to do a good job because the system is opaque. In response to the failings of liquidity renting, Obol recently committed to prioritizing Protocol Owned Liquidity (POL) with Arrakis’s industry-leading liquidity management infrastructure in 2026. Obol also executed two strategic treasury operations to deploy onchain liquidity — one for 1,706,309 million OBOL and another for 300,000 OBOL — in January and February.

Only a few forward-thinking projects are exploring onchain liquidity today. But the market is beginning to adapt to the new era.

Historically, token issuers have relied on rented liquidity. But this is problematic because it disappears and often creates sell pressure due to the way market maker deals are structured. POL, on the other hand, is “a permanent balance sheet asset,” Orth says.

While Arrakis’s market research has found that only a few forward-thinking projects are actively looking into onchain liquidity, our four micro case studies below show that the market is beginning to adapt to this environment. We selected each featured project based on their enduring appeal and revenue accrued, the relative strength of their tokens, and their focus on POL.

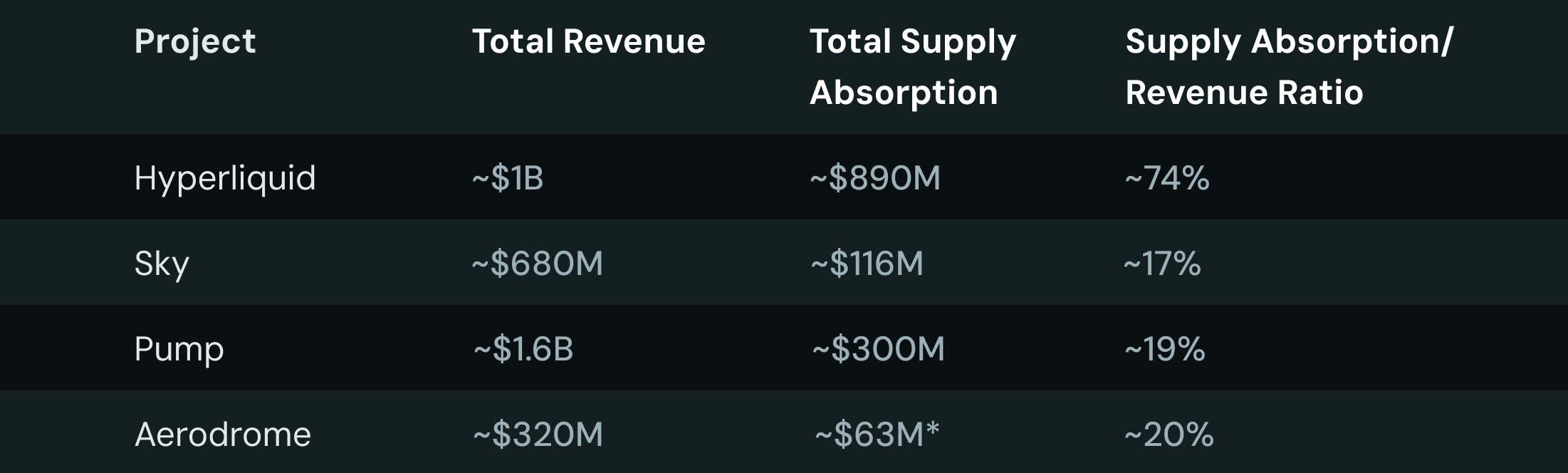

Supply Absorption refers to the amount of the project’s token supply removed from the market through strategic token purchases or locking mechanisms. Projects typically allocate funds using revenue from fees and occasional ecosystem funds.

Hyperliquid

Hyperliquid was arguably the biggest winner of the recent crypto cycle. HYPE is one of a handful of new tokens that’s outperformed BTC since launching and there are several reasons why. Firstly, Hyperliquid was a popular product pre-TGE with over $450 billion in perp trading volume. When HYPE launched, early users were generously rewarded.

It was also relatively difficult to acquire at the time because the team eschewed CEX listings until they reached out. As Arrakis’s A Practical Guide to TGE in 2026 found, CEX listings often weigh tokens down. This is especially true for projects that list on too many venues. “Everyone assumes more listings means more exposure, but it fragments liquidity and multiplies sell pressure through token allocations at each venue,” Orth says. “We found that tokens with fewer exchange listings have better month-one outcomes, suggesting over-listing may be a more common mistake than under-listing.”

Hyperliquid has also proven itself as a revenue-generating machine. The protocol averaged ~$80 million in monthly revenue in 2025, bringing its cumulative total revenue to ~$1 billion. Today, Hyperliquid directs almost all of its protocol fees into its Assistance Fund to accumulate HYPE, with ~$890 million spent to date.

Orth notes that profitable projects are increasingly adopting such mechanisms. “Revenue-funded treasury operations are becoming more commonplace, and they’re a structural counterweight to continuous sell pressure,” says Orth. “Protocols can now also run these mechanisms fully programmatically and non-custodially. But the prerequisite is revenue. Without it, these operations are just treasury drawdowns with marketing attached.”

Key takeaway: Revenue is a major driver for achieving sustainability and the leading teams are using their revenue to accelerate growth.

Sky

Sky is one of DeFi’s most profitable protocols. The USDS creator averaged ~$20 million in monthly revenue in 2025 and it’s been one of the ecosystem’s biggest earners dating back to its early days as Maker. Sky has spent a cumulative total of ~$110 million of USDS through its Smart Burn Engine at writing, allocating a portion of its revenue towards SKY purchases on a rolling basis. Sky also pairs SKY with USDS to build its POL, improving its onchain depths and execution. Like every major early-generation DeFi token, SKY trades below its 2021 peak at writing. Still, it’s emerged as one of the strongest performers in a market that’s been struggling since 10/10.

Though many projects are still reliant on rented liquidity, Orth is direct about the benefits of POL. “With POL, your liquidity is always there to quote even if markets go down, execution is fully verifiable onchain, and DEX liquidity you own cannot be revoked,” he explains.

Key takeaway: Forward-thinking teams are allocating their revenue towards POL to improve their onchain liquidity depths and token health.

Pump

Pump sparked controversy when it launched at a $4 billion FDV in July 2025. But few could fault the timing, with the ICO landing straight off the back of the app’s viral breakout during memecoin mania. Pump also introduced Project Ascend post-TGE, introducing dynamic fee tiers to incentivize small creators to keep their projects alive (and disincentivize rug pulls).

Project Ascend initially allocated 25% of Pump’s revenue towards regular PUMP purchases then increased the allocation to 100%, with ~$300 million spent to date. PUMP is down from launch with an FDV closer to $1.8 billion today, which implies the ICO’s critics were correct. Still, PUMP has been one of the token market’s strongest performers given the years-long washout.

Key takeaway: Teams win when they build products the market wants and capture the generated revenue.

Aerodrome

Aerodrome was an early entrant to the Base ecosystem, replicating the vote-escrow model that made Velodrome a success on Optimism. It quickly became Base’s top DEX by volume, outpacing the likes of Uniswap and PancakeSwap. In 2025, Aerodrome’s averaged ~$14 million in monthly revenue, which comes from fees that go to those who lock AERO into veAERO positions. The Aerodrome team has launched several initiatives to either directly acquire AERO or reduce the circulating supply. One of them is the Momentum Fund, which uses 100% of the team’s earned fees and bribes to acquire AERO on the market. The Momentum Fund has acquired ~10 million AERO to date with the total supply locked by the team sitting closer to 155 million AERO (the bulk of the locked supply comes from previously allocated incentives and protocol owned rewards). Most DEXs take a different approach towards revenue by directing fees to LPs. Many have also criticized AERO’s inflation schedule. But few teams have implemented measures to lock their token supply with such tenacity.

Key takeaway: Teams may use multiple strategies at once to reduce their token’s circulating supply and build their POL.

Our Reflections

In this case study, we’ve looked at how some of the strongest, most widely adopted projects in the space today are adjusting to the new token era. While these projects differ from one another in scope, they all share two similarities:

- They’re generating revenue.

- They’re using their revenue to build their POL.

This is because their teams understand that we’ve entered a new era. Many projects have not yet adjusted and their tokens are suffering worse than those on our list. But the shift in sentiment across the industry is palpable: everyone understands that it’s not 2021 any more and projects need real adoption if their tokens are to succeed.

It’s worth noting that current revenues are often a lagging indicator for projects that are early in their revenue growth path. Many token projects are early in their adoption cycle with projected revenues that could substantially increase over the next decade. For projects that are on a path towards sustainability, current revenues are not always sufficient for calculating their valuation.

As tokens enter a new era, competing projects are taking different approaches to revenue, creating interesting dynamics in the market. In the perp DEX space, Lighter partnered with Circle this month to share revenue from the $920 million in USDC deposited to the DEX. This is a different strategy to Hyperliquid, which moved to USDH last year, meaning it earns all of the interest from the reserves backing it (this in turn gets allocated to accumulating HYPE). Before the move, multiple major stablecoin issuers entered bids to become Hyperliquid’s de facto stablecoin on the project’s governance board, leading to a drama that ended with USDH securing 68% of the vote.

The death of liquidity renting accelerated the shift towards revenue and POL.

Over recent years, changes in the CEX landscape signaled that tokens were entering a new era. In crypto’s early years, CEXs provided a valuable service to token issuers because they enabled fast capital formation. But over time, renting liquidity from CEXs and market makers has become more and more costly for token issuers. Meanwhile, many new tokens have entered the market, onchain trading has improved, and a handful of assets have become liquidity magnets while most bleed. While liquidity renting did not kill alt szn, its death accelerated the shift towards revenue and POL.

According to Orth, projects with smaller treasuries stand to benefit most from prioritizing POL due to the cost of listing on CEXs versus the value they bring. “CEX volumes have a steep power law with Binance dominating against smaller venues. So if you’re not getting a top-tier listing, the cost-to-volume ratio may not justify the sell pressure,” he says.

For our part, Obol has taken steps to respond to the new market structure. In early January, we explained why we would be prioritizing POL moving forward. Building onchain liquidity allows us to improve liquidity depth, market efficiency and price execution without relying on external parties. We also launched the Obol Economic Engine last month, executing purchases for 1,706,309 OBOL and 300,000 OBOL to allocate towards our POL.

Tokens are not dead and the likes of Hyperliquid and Sky prove that. Alt szn, though? That’s a different story. As we said earlier in this piece, it’s not 2021 any more, and most tokens will struggle to achieve sustainability if they don’t focus on revenue and POL.

The data included in this piece was correct as of February 25, 2026.